Certainly, putting only a portion of maximum position on is a form patience. But I am suspicious of scale in trades on the short side. since there is no theoretical cap on the rally if you keep increasing your position as the market moves against you, you can still be squeezed out.

Expressing your view via Short ETF which is the same as put option, limits the downside but also incurs option costs and a risk that your capital your drain out, because of bad timing

Having said that, if you are right you are right. People do make money on the short side. Just much less than on the long side.

There has been a lot of talk about the bubbles lately. Stocks are a bubble or bonds are a bubble. Dollar is a bubble or all other currencies are a bubble. Bitcoins are a bubble or fiat currencies are a bubble. Start-ups are a bubble or established companies are a bubble. The list goes on.

All I know: the only thing worse than going bust buying into a bubble is going bust selling into a bubble.

For the purposes of this post I am going to assume that you, the reader, have a way to identify a bubble.

By identifying a bubble, in some specific security or in a market, I mean knowing with complete certainty that at some point in the future this security will trade at 50% of its current price.

Knowing some like this with certainty is a tall order. But I will give you this. There are instances of obvious bubbles/dislocations, and though the financial world is probabilistic, at some point you have to go with your own reasoning.

What I will not give you, is the knowledge of the timing of the said bubble bursting and the timing of this 50% price decline occurring.

Now let’s look back at the tech bubble of 1999-2000.

The NASDAQ peaked out at over 5,000 in March 2000 only to fall later to close to 1,000. One could argue that the bubble had been already identifiable when NASDAQ reached, say, 3,000 in 1999. Certainly, it subsequently corrected by more than 50%.

So who is a worse trader – the one who bought it at 3,000 or the one who sold it short at 3,000?

I don’t know the fate of a bull: it depends on the stop-loss strategy. But I do know the fate of the bear, and it is grim.

This is the problem of all short-selling strategies. You think a company as overvalued at $100 and set a target price of $50. But what if it goes to $150 before it goes down? Are you actually going to hold the position?

The answer might be “yes” for some people. Such people usually don’t survive in the world of leverage finance – your capital, your credit lines will eventually get exhausted and your investors will flee.

Of course, you can limit your downside by expressing your bearish bets via options. But this is a treacherous path as well. Downside options tend to be expensive and decay rapidly. The view might be correct, but your timing might be off, and the options will drain your capital before paying off.

All of us want to be John Paulson, who made something like $20bln betting against subprime mortgages. My hat is off to him and his team for their excellent research and unwavering commitment.

But even the people who correctly anticipated the mortgage crisis, didn’t have an easy time of timing the collapse or finding the correct strategy to take advantage of the bubble. For every John Paulson, there are a lot bear skeletons littering financial thoroughfares.

Am I telling you that there is no way to take advantage of recognizing a bubble?

No. There is one sure way.

SIT IT OUT.

If you know that stocks will collapse below current levels, stay flat! By the virtue of being in cash, you guarantee yourself a great buying opportunity (like in 2002 or 2009) with no risk of being squeezed.

Originally (pre-2005) it was undoubtedly true that China had kept its currency artificially weak. Since then the real appreciation (accounting for inflation) against the dollar has been very considerable. The real appreciation against China’s possibly most important trading partner – Japan has been tremendous.

It is difficult to say what Yuan value should be. I am inclined to believe that now Chinese currency ir artificially strong and is causing the loss of competitiveness. Free float and release of capital controls might lead to a massive capital flight.

1. I like short CNY – think it is a good long-horizon trade

2. Short AUD makes sense too, but AUD have depreciated a lot. See my most on Kiwi conundrum from earlier this year. NZD is possibly a better was of expressing this short.

3. I don’t like short S&P, because I don’t know how far it can rally before the next crash.

Comical failure – this is how I would describe the quest for 2% inflation by the developed world central banks.

So what is the Fed thinking, as it is gearing up to tighten?

In my post on February 8th and during my appearance on Wharton Business Radio @BizRadio111 on February 13th, I have argued that imminent tightening is the most likely scenario. I have focused on what the Fed will do.

Now I find myself drawn into the discussion of what the Fed should do. This question might be less important for short horizon trading, but it bears a lot of weight when you consider long-term policy implications.

Is the Fed too easy? Should we worry about inflation and asset bubbles?

Is the Fed too tight? Should we worry about deflation and recession?

Or are we in a perfect balance leading into a perpetual Goldilocks scenario?

Essentially, the Fed is trying to achieve maximum prosperity (whatever that means), while maintaining price stability.

The developed world somehow has accepted that price stability means 2% inflation. If we regard this notion as a starting axiom (or as a religious dogma), I believe the Fed is wrong.

Indeed, I see little indication that we are heading towards 2% inflation in a tightening environment. The USA has made a decent progress on growth and employment. But does this guarantee inflation?

I am not arguing against the fact that wage pressure could be inflationary. I am just not sure that there is a causality between economic growth and wage pressure. There certainly has been some concurrence of those things in the 20th century. But now we don’t see this concurrence. Why should we assume the causality?

My opinion is that labor having negotiating power was an idiosyncratic 20th century phenomena. Technology and globalization are leading to deep labor redundancy and increasing power of dynamic capital.

But even if I am wrong, and there is some wage pressure looming on the horizon, do we not have some serious offsetting factors? Rising dollar? Pull-back in commodity prices? Deflationary threat from China slowdown?

I am not alone in being “inflation skeptic”. And most people, who think this way, conclude that The Federal Reserve is about to make a mistake.

However, my own argument is making me see the other side. If I believe in unlimited technology-driven growth and labor redundancy, why should I believe in the 2% inflation target?

And is deflation really so corrosive? It was in Japan, but that was a different century. The risk of deflation is that people and businesses will wait to buy goods hoping to get a better deal in the future.

Are you waiting a few years for I-Phone 12? No, enough of us are buying any new tech as soon as it hits the market. Even if we know it will be 10 times cheaper and better in a couple of years.

The technology cost overall has dropped below the threshold when the utility of having always outweighs the utility of waiting,

One might argue: technology is not the whole economy. Well, some other areas of economy (like housing market!) could use a bubble control on occasion.

I do not have a firm conviction, but I have a strong suspicion: 21st century economy has capacity to grow without inflation. And in such robust growth environment the fiscal problems can be solved without resorting to inflating out of debt.

In this case there is a possibility that 1.6% inflation in the USA a sign of significant overheating. In this case the Fed does need to raise rates!

But what about the dollar strength? One could go both ways on this. Dollar has momentum, but it is not extremely strong by historical measures.

And The United States might be now in the unique position of strength, warranting even further currency appreciation.

I do think the Fed will raise rates. And I do think we will slide into a new recession thereafter. But I am not sure the future recession will be the fault of the central bank.

It is possible that making two wrong assumption (wage pressure and 2% target), the Fed will stumble into the new price-stability.

Historical ranges are a good guide for setting price targets. When the carry is positive I am willing to keep the trade longer – until the changing exchange rates will start affecting the respective central bank policies.

Interest rates markets may take many paths in 2015. My “central” scenario is that the Fed will start tightening this year as projected and the curve will continue to flatten, lifting the long end.

I don’t much problem with the Fed’s position – all they are risking that they will stop making money on Treasurys at the pace they currently are. But they have no reason to liquidate their holdings in a hurry. They control both the rates and the money supply.

I don’t have a date the book yet- approaching publishers now.

I prefer to focus on what the Federal Reserve WILL do, instead of what it SHOULD do. A lot of time is spent debating the latter, while what will make money for us, is understanding the former.

This post is designed to communicate some ideas about trading U.S. markets in the tightening and pre-tightening environments – something the younger traders might have not experienced. But first I want to make a case why Fed’s raising rates this year is a likely scenario.

The opinions on what is necessary for the economics are clearly divided. And I am not the one to resolve this debate.

The projection of rates going up sometime in the middle of 2015 dates all the way back to 2013. Since then the market gyrated, but continued to inexorably creep to this target date. September-2016 Eurodollar contract is good proxy for the tightening schedule anticipation:

While this contract has being going nowhere, the 2-yr swap rate, which indicates where we are on this consistent schedule, is steadily creeping up:

The Fed knows this. And they are not speaking otherwise. I think they are OK with this schedule. Low inflation and strong dollar notwithstanding.

Let me be clear. I do not propose betting heavily on the tightening, especially on a particular schedule. There are a lot of uncertainties in the world – a lot can go wrong in the next few months and deter the Fed.

My point is that the current course is set and the burden of proof is on the contrarians. In this context last Friday’s job report is especially important. Usually, I don’t put much weight on a single economic indicator, but this strong release came at a critical juncture. It took away a major opportunity for the Fed to diverge from expectations by claiming weaker economy or job market.

I think we should brace for the tightening to come and enjoy the ride.

Here are some lessons I have learned from the last two tightening cycles:

1. Yield curve flattening will start earlier than you think and will be more vicious than you think.

UNDER NO CIRCUMSTANCES EXPECT HAWKISH FED TO CAUSE LONG END TO SELL OFF.

This understanding allowed me to load up on the bonds in the end of 2013 (not as an allocation, but as a leveraged trade). If the Fed stood pat, I would be receiving the carry indefinitely, but when they started leaning towards hiking – I knew the long end would be supported.

2. No matter how much the curve flattens or inverts, the reality will be even more extreme than its anticipation.

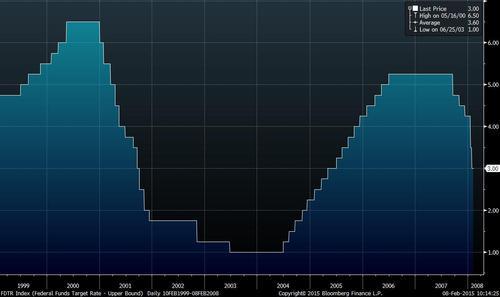

In 2006, someone told me that the easing of a cycle takes place on average only 9 MONTHS after the last tightening of the previous cycle. This sounded like complete nonsense. How stupid the Fed should be to tighten only to have to ease nine months later?

Well, let’s remember the hikes of May 2000 and June 2006. I don’t have to tell you what happened shortly after. Notice how short the “flat tops” of the Fed Funds target rate were.

So remember:

TIGHTENING LEADS TO EASING AND THE MARKETS WILL ANTICIPATE THIS TO AN EXTENT.

3. There is a lot of talk of how long (albeit lackluster) this expansion has been and for long we were in the equities’ bull market.

Well all this time we did not have hikes. The last two times:

TIGHTENING WAS FOLLOWED BY RECESSIONS.

So anticipate the stock market and the economy to roll over 2-3 years from the beginning of the tightening cycle. Given the unique current circumstances (dollar appreciation, China slowdown, European woes) those things might happen sooner.

So check the lines securing your portfolio. These are different seas.

In 1986 AUDNZD cross entered one of the greatest and easiest to navigate currency ranges of all times.

Buying the cross (i.e. buying Australian currency vs. selling New Zealand) around 1.05 has been a particularly easy (though very slow) trade. I used to be Mr. Aussie-Kiwi, so why am I hesitating now? Why do I have no position on?

First, I want to point out something which becomes obvious with a microscope: the range actually didn’t hold this time. The cross broke to new lows, around 1.035, before bouncing back to the current level of 1.069, as i am writing this post.

Some might think of such a breakdown as ominous, some as short-lived and unconvincing. I am not a technician and I would be inclined to think the latter.

The range doesn’t mean to me is not that there is some mysterious support level that may not be breached. Rather, I conclude that New Zealand economy is so tightly dependent on Australia that the exchange rate below 1.05 (i.e. New Zealand dollar stronger than 1.05 of Australian dollar) is just not sustainable.

What really gives me a pause that I am so suspicious of AUD and Australian economy. Why now?

Australia has gone without a recession for a really long time (most of the time in this range, in fact). The recent back up in commodities puts pressure on the Aussie (as Australia is a producer/exporter of commodities), but by itself it does not seem worse than other back-ups during the period on the chart.

The key new risk is the same factor which I think helped Australia to levitate thus far: CHINA.

If the signs of China slowdown we are observing will develop into a full-blown recession (or a currency devaluation), what will that do to AUD?

Now could Kiwi buck an idiosyncratic collapse of Australian economy and currency? Not likely. Though I have to consider falling energy prices and lower shipping costs favoring New Zealand as a food exporter.

Do you see now how I am getting pulled in different directions?

1. I am fundamentally bearish on AUD vs. USD, but it has already corrected so much from the highs, that I think there might be easier pickings in the long USD land.

2. AUDNZD is historically very low, but I am loath to put on any trade which would expose me to AUD.

3. I could go short NZD vs. USD directly as an enhanced version of short AUD. But I am once again running into: “This is just another long US dollar trade and I have plenty of those”. Also NZD trade has also moved quite a bit and to make things worse has negative carry.

4. I could consider a different cross to get better carry and exclude USD from the equation: MXN/NZD? TRY/NZD? BRL/NZD? I would be going into the land unnecessary complexity and idiosyncratic EM risk.

So what do I do? I think.

My core strategy of being long dollar and long US bonds has been working its magic. When things are very good for a protracted period of time, it is wise to reduce risk. So I am not committing capital, unless I am very sure of my strategy.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Google Analytics and Tag Manager

This website uses Google Analytics to collect anonymous information such as the number of visitors to the site, and the most popular pages.

Keeping this cookie enabled helps us to improve our website.

Please enable Strictly Necessary Cookies first so that we can save your preferences!