Or, more importantly, in my portfolio.

My readers know where I stand: long Treasury Bonds, long dollar.

I am not perturbed by strong employment report. In fact, on February 8th, after the previous report, I wrote a piece advocating that the Fed was on the tightening track.

True, even this Friday’s report can be interpreted in more than one way. Some prefer to focus on weak growth in hourly earnings, rather than on the headline.

I will stick to the facts I know. The market is pricing tightening and the Fed is not saying otherwise. The last two unemployment reports are certainly not derailing the tightening train.

I welcomed the violent sell-off that occurred on Friday. I was waiting for such an opportunity to double-down on bonds.

My logic is:

For now the dollar rally will compensate me for any losses from rising rates. But as the Fed hikes, the curve will continue to flatten and sooner or later we will be pushed into a recession. When the economy rolls over the bonds will rally again.

Meanwhile, I also rely on the fact that Europe and Japan are boxed in the QE-induced environment of zero to negative interest rates. A hiking cycle will widen the rate divergence, fuel further dollar rally and cause deflation. Right?

Contemplating the recent price action, I have become concerned. We have grown accustomed to negative inflation surprises from Europe and to the idea that whatever QE they will schedule, even more will have to be done.

But bond markets always act like they can’t go down. Until they do. And then they really do.

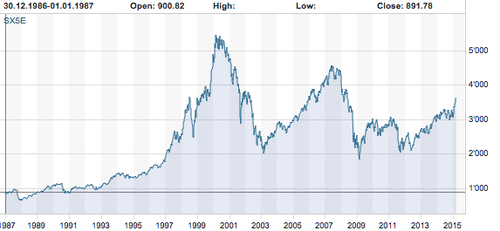

Euro has corrected by over25% and EuroStoxx 50 certainly thinks that the economy is getting traction.

What if the market suddenly decides that Euroland is on the path to reinflation? And Bunds decide to back up say 200 basis points? What would provide a cap on US yields? And if the global bond rout is Europe-driven, will the dollar hold up?

I actually don’t think this will be case. The Emerging Markets are too fragile now. In particular, I think that a significant rise in Developed Markets yields would push China over the brink.

So China slowdown is a safety net against bond collapse and dollar trend reversal. But China has been bucking economic doomsayers for over the decade. Could the net prove to be flimsy?

To summarize: I suspect that market participants, including myself, are not prepared for a dramatic change of rate sentiment in Europe. Therein lies the fault line in the global bond markets.

CIO, HonTe Investments. Ran global macro at JPM. Yahoo! Finance Contributor. Ph.D. in Mathematics. Author, The Next Perfect Trade. No investment advice.

{kind=link}

{kind=link}