Market

participants, remembering the impact of Brexit, have their focus on France this

weekend. The last thing I want to do is add into the

mix my futile hunches regarding the probabilities of various winning candidate

permutations. Furthermore, wI won’t even speculate how the market will react to

any particular second round match-up.

The purpose of

this note is to discuss a rare, tactical conviction over this weekend.

Staying COMPLETELY AGNOSTIC as to whether the election outcome will be taken as

Eurozone positive or negative, consider USDCHF.

Scenario I

The outcome is

perceived as negative; fueling French EU exit fears (‘disenfrancising’) and

risk-off trades such short USDJPY, short equities, and long US Treasury bonds

are expected to benefit. EURUSD is likely to fall and underperform CHF.

However, given the close linkages, CHF is likely to be dragged down by the EUR

and, unlike JPY, underperform the US dollar. So, in this scenario, we expect

USDCHF to gain.

Scenario II

The outcome is

perceived as positive; risk-on trades, such as long equities, are expected to

benefit. US and European risk-free rates are likely to trade higher. EUR

will likely outperform CHF and possibly by a lot, as Swiss interest rates are

more pinned, and USD will rally against safe harbor currencies such as JPY and

CHF. So, in this scenario, we expect USDCHF to appreciate.

To

re-cap, USDCHF

goes up, or USDCHF goes up.

It is

important to underscore that when I talk of tactical conviction, I don’t mean

“I am positive that this

trade will make money,” rather I mean “I am convinced that this is a positive expectation

trade.”

Markets are

finicky, and even with the logic above I can assign no higher than 60% chance

of being correct.

And we I am fully prepared to be completely wrong.

Hence, I am purposefully posting at the end of the trading day not to entice the reader to

follow our trade, but to share and “timestamp” my thinking, which typically

applies to the long investment horizon, but in this unique case may have a

short-term value.

For

over two solid weeks after the election, the markets have been relentlessly

pricing in the success of “Trumponomics.”

To be clear, we mean “success” in a purely non-partisan manner. It just means the President-Elect would accomplish what he says he is going to

accomplish, whether that might be good or bad in an individual’s view.

Furthermore, we discuss economic causality only to the extent it affects

financial markets, or more precisely, how it defines superiority and dominance

relationships between specific trades.

With

that in mind, let’s start untangling Trumponomics with its flagship item:

infrastructure stimulus. Long on the Democrats’ agenda, the package of $500bln

to $1tln is now expected to pass through the Republican Congress. Without

offering our amateur political analysis, we point out that this may or may not

happen.

By

“expected,” we mean the price action in:

Equities;

Industrial commodities; and

Inflation break-evens.

Surely,

if the stimulus were to pass, all else being equal, it would provide a tailwind to all of the above. But, the

magnitude of the move thus far has already been substantial enough to make us

question if betting against the stimulus is taking on a characteristic of an “Even If” trade discussed in Chapter 13 of The

Next Perfect Trade. The argument being that there are occasions when the

market pricing is so skewed towards one outcome, that betting on the opposite

outcome may make money even if

the most expected event comes to pass.

The

recent price action in pertinent markets:

US Equities: 1m Historical

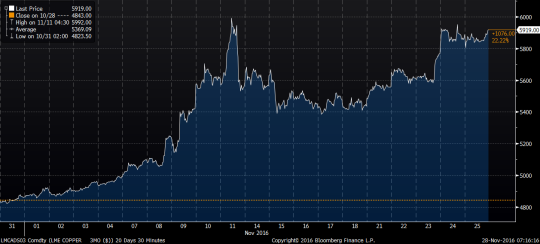

Copper:

1m Historical

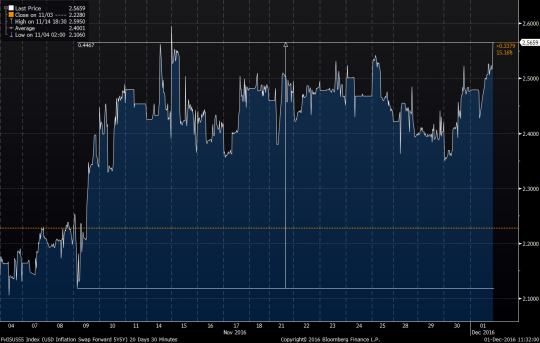

5Year US Inflation Breakeven: 1m

Historical

FED

Response

Now

let’s shift the discussion to the Federal Reserve. Should the stimulus pass,

the Fed would consider the rising inflation expectations justified, based on

the triple impact of:

Rising commodity prices;

Tightening labor markets; and

Wealth effect from the stock market.

Importantly,

the Fed was well on track to tighten imminently regardless of the election

outcome, so in this case the EVEN IF trade points us in the direction aligned

with Trumponomics. There have been debates on whether the current Federal

Reserve is too tight or too easy. We elected to stay on the sidelines but

consistently highlighted that the Fed is indubitably hawkish relative to other DM central banks.

Though

Trump criticized Yellen during the campaign, we are not sure how much of that

was purely political rhetoric, and what he would rather she do or not do. What

we know is that Ms. Yellen is likely to stay on for the remainder of her term

and to pursue her policy framework. As for what

comes after, we would posit that the President-Elect has a good understanding

of debt and interest rates; he would likely “push” for a policy that would

neither stifle the economy through excessive hikes nor allow inflation

expectations to run away leading to a catastrophic steepening of the borrowing

curve.

We

pointed to the limitations of the curve shape as a leading indicator in our

post, Flat

Curves & Recessions, from September 28th, but steepening is

often viewed as a good thing as it is associated with periods of solid economic

growth. On the other hand, as the United

States has a considerable current account deficit, higher rates are net

negative for the wealth of the nation (more interest going to foreigners), and

this is something Trump may be aware of.

Overall,

we see no reason for the new administration to nudge the Fed to one extreme or

another, so ‘business as usual’ is our best guess.

What Does This Mean for The

dollar?

The

US dollar (USD) has strengthened a lot on the back of Trumponomics. This price

action is consistent with the notion of a

reasonably vigilant Fed, which would raise REAL interest rates in response to

higher inflation expectations.

USD: 1m Historical (DXY)

Recent

re-price of the markets notwithstanding; we continue to maintain that

stronger dollar is a concurrent necessity with

respect to higher interest rates. In other words, if US rates stay where

they are or move higher, the USD should continue to perform well on a total

return basis. For those who feel that the dollar rally has gone too far, we would refer to our post

from March of this year and point out that given the rates differentials,

the current 10-year forwards in EURUSD,

USDJPY, and USDCHF are 1.3150, 84.00, and 0.7500, respectively.

As

we have long noted, ECB, BOJ, and SNB do not have to ease further to weaken

their currencies; all they have to do is to hold steady and let the Fed lift

off.

Most

dollar bears base their view on the implicit necessity of the US rates playing

out much lower than currently projected. Our logic then dictates that betting

on lower rates is the dominant trade.

Let’s

Talk About the Transmission Mechanisms

Higher

rates and stronger dollar traditionally are seen as a recipe for a deflationary

slowdown.

As

an aside, we acknowledge the point of view that in a stronger final demand

environment, higher rates may, in fact,

be inflationary as they increase the production costs. We, however, stick with

the simple perspective that real rates are “the cost of money.” And if the cost rises, well then money

becomes more expensive, i.e. deflation. Of course, a further nuance may

be possible arguing that higher rates are mostly deflationary for asset prices,

not consumer goods – a theory well supported by the fact that recent low rates

have helped asset prices much more than wages.

We

are acknowledging those arguments to emphasize serious uncertainties and

complexities in the rates mechanism, but we will stick to the simple

observation that “too high rates” typically lead to a collapse in the stock market, which is often followed by an economic slowdown.

We

have long argued for the negative predictive power of interest rates and that

perpetually upward sloping and steep

yield curves, provide a tailwind for the secular bond bull market.

The

dollar rise should be even less controversial, as it incrementally leads to

weaker exports and lower imports prices.

So,

on an “all else being equal” basis, the recent shift to higher rates and stronger

dollar equates to a tightening monetary condition and should lead to lower

inflation expectations, a flatter yield curve,

and lower equity prices.

This

transmission mechanism is challenged by

the market’s acceptance of the Trumponomics. The higher rates would be offset by the stimulus and the impact to trade from a higher

dollar by import taxes. Tariffs being another “may or may not happen”

proposition. We will not even go into

the risk of a global slowdown caused by potential

trade wars.

It

is sufficient to say that the tightening of economic conditions is present here

and now, and stimulus and tariffs are

something that might happen in the future and just might have the expected

effect.

As

you may guess, we continue to argue for

our portfolio strategy; a combination of long US bonds and long US dollar

against DM currencies.

When

addressing bonds, it is important to

mention the credit risk which may increase

with Trump’s potential expansion of the budget deficit and his rhetoric,

however unlikely, regarding a “workout” on the US debt.

Long-dated bonds have cheapened significantly

over the last few days on an asset swap basis, some of them approaching the

level of Libor + 60 bps. Some have viewed that relationship as mathematically impossible

and attribute it purely to technicals related to the Dodd-Frank limitations of

balance sheet and foreign CB selling.

As

we wrote in a blog post a year ago, it is not exactly as simple as that.

However,

setting technicals aside, the only economic justification for the current levels is the pricing of at least 100bps of credit risk. This, in itself, implies something like 80

cents on the dollar workout on long-dated

bonds, which in our view is extremely conservative.

There

is no doubt that the Trump victory has introduced more uncertainty into the

rates environment, but we are well compensated

for this. For example, while we would

rather be long bonds with Clinton than with Trump at the same level, we prefer

to be long bonds with Trump for an extra 100 bps.

And

finally, for what it’s worth, both the magnitude and velocity of the recent

correction are entirely consistent with

multiple, recent corrections including:

Short JPY, CNH, and NZD are three currencies positions that have been prone to elicit doubt and second guessing recently.The great JPY short (long USDJPY) initiated as early as 2010 is much discussed in my book. Through 2015 it satisfied many characteristics of a superior trade.

Short CNH (long USDCNH) and NZD were also added to the portfolio in early 2015. Several of my blog posts discuss the favorable risk-reward of those trades, especially USDCNH.

The common theme between these three trades is that all of them were initiated based on very solid strategic considerations and had delivered excellent profitability until recently. Over the past several months, all of them experienced a significant draw-down and/or a pickup in volatility. And all of them had experienced a meaningful challenge to the concept of their individual superiority.

Yet in all three cases, I have chosen to stay with the trades, albeit with differentiated risk exposures. In this piece I will discuss the various considerations that ultimately lead to this decision with regards to JPY.

Entering long USDJPY in the low 80’s and pyramiding it as the momentum built, I had established clear price targets; 110 in the event of a stable dollar and 120 to 125 in the event of much broader dollar strength. Price targets are to be respected and I dutifully took profits around the 120 level. In fact, by the end of 2015 my exposure to USDJPY relative to the size of my portfolio was less than 15% of what it was at peak exposure.

Whether it was correct to get flat or to run the residual position to see if the market would overshoot was, without the benefit of hindsight, neither here nor there. The true strategic question was what to do once the significant correction in USDJPY had occurred.

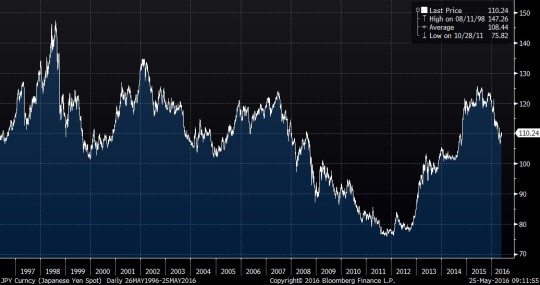

20yr Chart of USDJPY

Based on the chart above, it is not clear whether the cyclical trend is sustained. As for the secular trend, it is more favorable for yen on a price basis and slightly more favorable for the dollar on a total return basis.

With respect to specific asset valuations, Chapter 1 of my book discusses the importance of a currency pendulum, which is propelled by economic gravity. Such gravity is often manifested by a central bank policy.

So is the recent change in USDJPY direction a sign that the pendulum has started to swing back the other way? It is important to remember that CB talk and incremental policy adjustments are more important in terms of changing sentiment than fundamental flows.

Indeed, every speculator encouraged or discouraged by the BOJ, who sells USDJPY, is the speculator who later has to buy USDJPY. And since our time horizon is longer than that of virtually any other market player, the net long-term effect on our portfolio is minimal.

Spec JPY Positioning (CME, Non-Commercial Futures, >0 = Long JPY, Short USDJPY)

However, the actual policy does have an effect. A central bank is a monopolistic issuer of its own fiat currency. And continuous increase of supply is bound to make a product cheaper.

The fact remains that the BOJ is continuing to buy assets and add liquidity and the FED is not. Furthermore, I see no imminent change to this situation.Thus, I find it hard to imagine that economic gravity would change against the dollar, unless the Federal Reserve policy were to change dramatically. Our long bond position should take care of such an eventuality.

For now, I regard the recent yen strength as a correction of a trend over-extension. Staying long USDJPY through such a correction has a logical implication. We are supposed to add to the position if it goes further down.

I try very hard to avoid the fallacy of trying to pick an exact “floor” for the price. If it went down to 108 there was no reason to be sure it couldn’t go to 106 (and it did!). But since our core thesis is based on policy, such price action should encourage us to increase the position rather than stop out.

As one of the superiority tests for this trade, let us check if its opposite is a “self-defeating chicken” (strategic language from Part III of my book). We don’t know whether USDJPY has currently bottomed close to 105 or whether it could go to 103, 101, etc. But what we really care about in terms of portfolio risk management are much more extreme scenarios. For example, can USDJPY trade back to the lows of 2011? I think that is highly unlikely. Further JPY appreciation would elicit such a raging policy response from BOJ that the resulting pendulum forces may propel USDJPY to new highs.

Some may disagree. There is an opinion that BOJ is powerless now to weaken their own currency. As I stated before, I am convinced that a CB can always devalue their fiat, as long as there is political will. People may argue if there is such a will at 110, but I assert that there WOULD BE such a will at 90. Thus as a sign of superiority USDJPY appears to have more upside than downside, as a large move to the downside creates a large opposing force.

Another superiority test is analyzing the historical pattern. What actually happens to USDJPY during US tightening cycles? This test comes back mildly encouraging. While having performed well through the 2004-2006 cycle; USDJPY fell sharply during the tightening of 1999 and started to riseonly at the last stage of the cycle in 2000.

But how can we can we tell, without the benefit of hindsight, where we are in the cycle? My preference is to remain agnostic about timing and to stick with what I know: eventually long USDJPY tends to win through the entire tightening cycle on a total return basis. Not the strongest endorsement, but an endorsement nonetheless.

Lastly, comes the dominance test. Assuming that we like long USDJPY, we must check if there are any trades across asset classes which are strictly dominant; that is, they would perform in every case when USDJPY goes higher and possibly in some other cases?

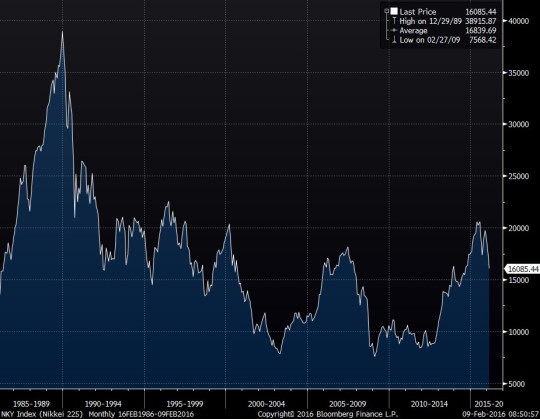

The most natural candidate for such dominance is Nikkei. Will the Japanese stockmarket go up in every case when JPY weakens? Not entirely certain, but the likelihood is high. Furthermore, Nikkei has recently started to show signs of performing when the yen is merely stable, as opposed to falling. Dominance is not established, but suspected.

Conclusion: Long USDJPY is still an attractive trade with attributes of superiority, but it is at a risk of being dominated. Long Nikkei holds its own attraction to us (see my post from February 10th, 2016) and appears to be incrementally favored by the relationship of concurrent necessity. Hence, USDJPY is a “hold” based on the policy support with modest tactical trading, while long Nikkei is an “accumulate” with an eye towards a significant position for the next great bull market.

Of course, timing is important but I don’t stake the success of my portfolio on the correct interpretation of technicals, flows and volatile indicators. As I discussed in Part II of my book, I trade when I see a clear extreme value and trying to time may only muddy up my risk profile.

Due to a large bond futures position, my portfolio has been trading with a strong risk-negative flavor for over a year, while in 2014 the long dollar and long equities provided a better balance. The fact that I am beginning to fish for cheap risk assets doesn’t signify a bottom is here or even close. Given my view that the China unwind is only beginning, I am inclined to expect that global financial markets will get even more dicey. But as I have said, I don’t like to over-invest in such directional bias. Risk may bounce and I don’t want to be forced to chase.

In Part III of my book, I discuss my principals of portfolio construction. In abbreviated form, rather than have just trade A pointing in the direction of my view, I prefer to have superior trades A and B pointing in the opposite directions.

My intention is not just to make a lot on one trade versus lose a little on the other. Rather, I plan to make money on one trade NOW and make money on the other trade LATER. So when I look for a risk asset I want to find something that may go further underwater first but is likely to emerge profitable. Indeed, not ALL risk assets rise from the ashes and investors need to show deference to secular changes. Consider Citibank.

In the 1990’s, the firm was a great buy and every dip was an opportunity. However, in the 2000’s it DID get wiped out – diluted beyond reasonable hope of recovery.

Well, that’s an individual stock market example. The broader market in the USA tends come back with the vengeance after every few years of meandering. Even the Great Depression which followed the 1929 peak took “only” 25 years to be redeemed.

But is this pattern true of global stock markets? Definitely not to the same extent. Nikkei is now over 35 years from the peak and nowhere close to making new highs.

Yet when I look in the mirror like Larry the Liquidator, played by Danny Devito in “Other People’s Money”, and ask “Who is the fairest of them all?” I am beginning to suspect the answer will be Japan.

The Nikkei may be positioned for a multi-year run to the new highs. Before I go further, I reiterate that China unraveling is a big risk to Japan but this is exactly the risk I am NOT worried about because I ammlong USTs and short RMB. I only need to be concerned with scenarios where China does ‘OK’ and the world doesn’t fall apart.

Three reasons I particularly like Nikkei and note that none of them are the introduction of NIRP.

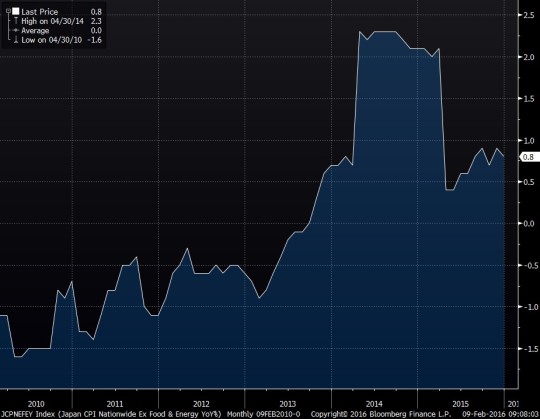

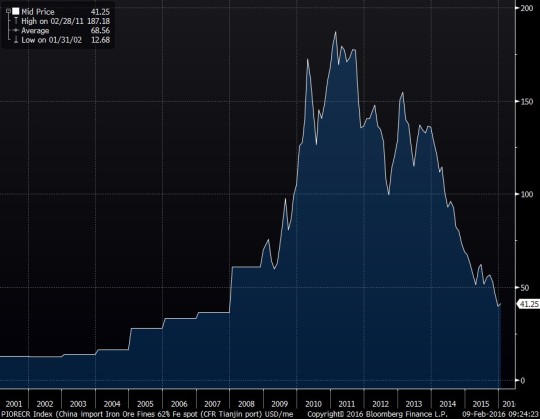

I. Core inflation is rising and this is good for nominal profits. I often scoff at “core” inflation in theUSA positing that energy is as important as any other CPI input. But Japan is different because unlike US, it is a pure importer of oil. And steel.

Japan CPI Nationwide Ex Food & Energy YoY% (VAT spike notwithstanding):

Iron Ore Prices, USD/Metric tonne [China Import Iron Ore Fine 62% FE Spot (CFR Tianjin Port) ]

A simple prospective of the wealth of the nation makes me bullish as they buy their inputs more cheaply and, due to the weak currency, sell their products expensively.

The recent upturn in the JPY shouldn’t cause a big problem given that the BOJ policy is likely to contain the Yen rally from extending. But even if the Yen strengthens further, a strong and stable domestic currency is a good thing, unless it’s TOO STRONG which is unlikely.

II. Japanese demographics may have a silver lining. An interesting point brought to me originally by @WorthWray is that the country’s aging population and declining labor force may prove to be a blessing in disguise. Shortage of labor pushes Japan to build on its strength: robotics. Japan is less likely to experience a backlash from job elimination caused by automation.

III. Regional instability. The last somewhat grim point is mine. I see a high likelihood of economic destabilization in China leading to political destabilization. As stated above this is probably not good for the Nikkei in the short run, but there is potentially a significant, long-term benefit. If crumbling China becomes externally (or possibly internally) aggressive, it will destabilize the entire region. That means a carte blanche for Japan to RE-MILITARIZE. And military build-up is usually very good for the stock market.

Good luck catching falling knives and keeping Band-Aids handy!

I’ve been somewhat prematurely congratulated on the success of my China strategy. Indeed, I have been vocally sceptic this year about Chinese stock market and currency. And given that I ALWAYS put my money where mouth is, it is natural for my followers to assume that I making “fortunes untold” on those trades.

The reality is that the trades I have been involved in this year have been, while profitable thus far, were by no means “slam-dunks” and may yet end being in the red.

The readers of my book “The Next Perfect Trade” http://tinyurl.com/q3sdqpo have pointed out that the long USDCNH trade, for example, may not meet some of my criteria for a superior trade.

My book had been mostly completed before China came into focus. In this post, by popular demand, I will outline my approach to trading RMB and $FXI in the light of my broader strategies.

As far back as 2006, I have started to suspect that Chinese economy was a giant Ponzi Scheme destined for a collapse far more devastating than what happened to Japan in the 80’s.

To be clear: I don’t produce my own economic research, all I can do is listen to people and side with those who make more sense.

However, for years I have stayed out of betting against China, because I couldn’t formulate any bearish strategy that would fit my criteria. I’ve written before how difficult, in general, it is to be short a stock market and as for the currency – the appreciation trend had been overwhelming.

I have mentioned in my book that if you can’t a find a good trade to express a view, you may want to question the view. So despite, having a wrong view for almost a decade, I have escaped much damage by failing to find a trade fitting into my strategy.

By 2013-2014 the China troubles appeared more imminent to some experts, but my eyes were turned elsewhere. I saw tremendous value in being long dollar vs. yen and, later, vs’ euro. But my strongest conviction was in the long end of the US Treasuries curve, where I had a disproportionate risk concentration by the beginning of 2014.

According to my strategic language (which I explain in detail in my book) being long USDCNY (betting on RMB devaluation) was, while attractive on its own, a strictly inferior trade with respect to other positions in my portfolio.

For the currency devaluation to occur, at least one, if not both of the following conditions had to be concurrently satisfied:

Broad dollar strength

Dramatic weakening of Chinese economy

My portfolio was already directly aligned with the first condition; and a massive Chinese slowdown was likely to affect the global risk appetite and cause a flight to the US bonds. Thus, in 2014, the currency bet was redundant to my portfolio and I stayed out.

In 2015, the game had changed: the dollar had already rallied and so had the bonds, making those bets no longer as superior. I was increasingly convinced by the arguments for the necessity of the Chinese credit cycle unwind. (I will omit the discussion of idiosyncratic pros and cons – I have written on the subject enough and for further information read “A Great Leap Forward?” by John Mauldin and Worth Wray.)

Yet I was waiting for another shoe to drop: the stock market. I thought Chinese stocks screaming up would give the government a good excuse not to devalue. Yet without devaluation the equity bonanza was likely to end in tears.

So I got involved in two very uncharacteristic trades: long USDCNH (offshore bet against RMB; at this point it appears I might have done better with USDCNY) and short FXI (Hong Kong listed Chinese large cap). I chose to bet against the dollar expressed ETF, because I was hoping for an additional benefit in the event of currency devaluation.

But Chinese stocks were rallying and I had no intention to be wiped out by shorting into the bubble (I’ve written about this too). So my only “option” was to buy puts, illiquid and expensive as they were. And as the market continued to rally another 25% since I started, I kept adding more puts, but I was beginning experience pain.

Why would I get involved in buying options and in betting against a currency with positive carry? I have cautioned against both of those things in my book. There are times though when the risk-reward appears so skewed, that it is beginning to have the flavor of a “free lunch”. I decided that the opportunity was too great, and in the absence of the ability to structure a “no-lose” trade, I had to risk some fixed amount of capital.

Initiate the positions and run them to the bitter end. No hedging, no whining.

Not only my long dollar/long bonds came under pressure in Q2 of 2015, but the capital committed to bets against China was grinding away. Fortunately, I had been positioned with enough caution to keep all the trades.

Needless to say in Q3 things got much better.

But I want to emphasize that my entry points were not perfect and the trades are far from complete with my portfolio still leaking carry and decay. In fact, the extreme scenarios, I have been hoping for, HAVE NOT yet materialized.

The equity trade I think will be over soon one way or another. But I still see no way out of further currency devaluation, and I will continue to pay carry to stay in the trade. With the full understanding that the whole strategy may yet end up being a loser.

In my book the “The Next Perfect Trade – the Magic Sword of Necessity”, which is now available on ebookit and amazon, I take the reader step-by-step through the process of selecting trades that are aided by market tailwinds. Broadening your range of success is the focus of my portfolio approach.

Also, I recorded my newest interview with Raoul Pal on RealVisionTV (my first interview is available for free on its site using this link; for the latest one you’ll need to subscribe but I find its content invaluable so please take the step to sign up using promotion code “Alex”). It was an excellent chance to review the concepts I was pondering as I was writing the book over the last year, and apply them to the current turbulent markets.

There is no longer an easy equivalent of the logically irrefutable long dollar/long bond trade of 2014; however, chaos breeds opportunities. What does my current investing strategy dictate?

The approaching Federal Reserve meeting is the most contested one in years. In the past, I worked hard to predict the exact path of the Fed Funds, and I was not bad at it. But nowadays I often feel that there are bigger fish to fry.

Some people think they will tighten several times in a row and some people think they are not tightening in our market lifetime. Let’s accept this uncertainty and try to come with a portfolio which will work regardless.

Long-dated bonds were my beacon through this cycle. Again and again, I have been repeating the mantra:

No hike means bonds earn carry

Hike means stronger dollar, curve flattening and long bond rally

Another beacon of value in the times of stock market correction, may be cheap, established technology companies that are unburdened with excessive debt and have proven to be able to adjust to the change.

On the other hand, the world of currency trades has shifted from “slam dunks” to merely “good risk-reward propositions”. My significant bets on weaker euro, yen, Swiss Franc, and yuan, after the original surge, have meaningful downside.

Chinese currency devaluation is coming into focus. I am inclined to stay with the trade as I can’t imagine any other way to stem the tide of capital outflows.

I have to face that sitting here today having little conviction about the direction of the stock market or economic growth (both domestic and global). This doesn’t mean I can’t have a position.

In my book and in my recent interview, I explain how I rely on my understanding of causality chains between various asset classes, rather on predicting the market direction.

So don’t get flustered by volatility. Take a deep breath, and instead of aiming for the narrow target of precisely anticipating the price action, look for trades that will succeed even when your views are wrong.

Like the old Soviet Regime, certain market regimes seem to be entrenched so thoroughly, that it is impossible to visualize any mechanism, by which they can be dislodged. But the Soviet Union fell and did so in a fashion few could have foreseen.

Until only a few years ago, Japan appeared to be caught in the never-ending purgatory of deflation, sagging growth and capital markets, and meaningless reform promises. In 2012, the current account surplus was not scheduled to elapse for a few more years, and the market flows, according to strategists, continued to support the yen. And then the sudden collapse of DPJ and Abenomics. You know the story.

And you also know the story of the Swiss Franc. First it was immovably pegged at a too weak 1.20 exchange rate to the euro. Then the immovable and indestructible peg suddenly evanesced. The franc briefly rallied above parity, which was way too strong. It appeared that the SNB had no means to control the currency appreciation. Until they did. And guess what? EURCHF drifted to somewhere in between 1.00 and 1.20. Probably where it should have been to begin with.

You probably can see where I am going with that. If general economic principles and historical patterns dictate that something has to happen, it probably will. Even if you see no possible mechanism to drive the transition.

I reviewed a book by John Mauldin and Worth Wray A Great Leap Forward?

I conceded that both China bulls and bears were making strong points. And with regards to currency I was giving heed to both those who said that a massive devaluation was inevitable and those who pointed out the imminent deval was neither necessary nor in the interest of the government.

There were few precedents to establish how price and credit overextensions unwind in tightly controlled communist/capitalist markets.

Personally though, I leaned to the bearish case for both equities and currency, based on the historical pattern for countries with credit growth excesses. Until proven wrong, I had to assume that the “what” of the equities correction and currency deval, even if I didn’t know the “how”.

And given that I ALWAYS put my money where my mouth is, my strategy did not permit me not to trade accordingly.

It was not cheap and my timing was not perfect. And today it is too early to celebrate victory: all my gains are reversible.

Now what? Do I stick to my guns and expect more of the same?

If you were wondering why I haven’t posted any anything extensive on the RMB devaluation thus far (I suspect you have better things to do than to wonder why I don’t post): I had relatively little to contribute to the discussion. I don’t have a clear idea why they did what they did and what their long-term plan is.

So in the absence of such insights, I have to stick the fundamental principle which drove the China trade, as well as other examples above:

Unsustainable will not be sustained.

If you see a major dislocation what have to bet on it eventually being rectified, even if you fail to understand the mechanism of the shift.

One of the reasons I prefer simple directional trades is because the “what” of the market is often easier to discern than the “how”.

And with the respect to China, if (and that’s a big if) you believe that the major dislocations are still there, it is reasonable to assume that they won’t be fixed by a 5% currency move. And so, regardless of what the authorities may have in mind, the odds are skewed towards further devaluation.

Chart source: Yahoo! Finance

Image: The Unstoppable Wave by Theophilos Papadopoulos

It is safe to assume that there will be a global deflationary shock wave resulting from Chinese stock market crash and trading freeze-up. Hard to imagine recent events to have no effect on consumption and investment. Recent fall in commodity prices is an example.

In this post I will go over a few world currencies and their connection to the recent events.

USA:

Facts: US job market appears to be steadily improving. The Fed exited the QE program and is contemplating a timeline for tightening.

Opinions widely differ and how well the economy is actually doing and whether there is any imminent inflation threat.

Currency: Long dollar continues to be the theme as it is favored by the policy divergence and spiraling pressure on the Emerging Market and falling commodity prices.

Euroland:

Facts: The economic performance appears improving, but there is no immediate threat of inflation. Greek crisis postpones any possibility of slowing down the QE.

Opinions differ on the full outcome and impact of the Greek debacle.

Facts: The economy has slowed down from its earlier tremendous pace and needs to work out some imbalances. The stock market is going through a massive correction and extreme volatility.

Opinions differ on how sound the overall economy is and on the necessity of the RMB devaluation.

Currency: Outright and options bets may offer a positive risk-reward as the potential for significant devaluation appeares underpriced. But there is no certainty of success and high likelihood of getting the timing wrong. Betting on the currency requires a strong China view.

Japan:

Facts: The inflation target is still not achieved and the economy is still struggling to accelerate. The QE is in progress and current government and central bank are extremely committed to achieving their inflation targets.

Opinions differ about the country’s economic future.

Currency: As short-term panic typically cause a flight to JPY as one of the “safe haven” currencies, I see any dips in USDJPY as an opportunity to build long USDJPY position. Indeed, Chinese slowdown is deflationary, and of all the central banks BOJ has the prime political mandate and tools to fight deflation. So the market’s tendency to strengthen the yen during stock market dips is completely counter-economic and a good entry opportunity.

Australia:

Facts: The economy is experiencing headwind from the China slowdown and falling commodity prices.

Opinions differ on whether the currency has reached an attractive valuation after the recent plunge.

Currency: Any bets the AUD have a strong component of expressing opinion on Chinese economic growth.

Emerging market:

Facts: Producer countries are suffering from falling commodity prices. The broad dollar strength is putting pressure on all dollar-funded carry trades.

Opinions differ on whether countries like Brazil or Turkey now represent value.

Currency strategy: I believe caution is still in order when investing in EM as the trend is abysmal, but if your portfolio is overall crisis resistant, some bottom-fishing may be in order.

South Korea:

Facts: Japanese currency weakness and Chinese slowdown are both deflationary for their neighbor.

Opinions differ of the overall economic health and debt problems.

Currency: I think KRW is on one-way train and this train is not going North. The current environment seems to offer very low chance of significant KRW appreciation. I am in favor of long USDKRW.

To summarize: long dollar vs. USD, JPY, and KRW seems to be a good risk-reward proposition regardless of the crisis outcome.

It has been a fun weekend. Between the escalation of Greek crisis and the surprise liquidity measures in China, it was as if the market never closed.

When considering market significance of a geopolitical event, it is important to distinguish between

The actual economic effect

The immediate impact on market players

In the case of the on-going Greek debt crisis and the potential so-called “Grexit”, remember that Greek economy commands only about 2% of the Eurozone GDP. Whether Greece muddles through or exits, the long-term economic impact should be moderate.

Two points that have been made by multiple people:

Greece exit might create a blueprint for an exit by other countries on the periphery, such as Portugal or even Spain.

Eurozone might be actually economically better off and the euro incrementally stronger without Greece.

What concerns me now though, is whether whatever happens in Greece may trigger a market panic or even a new crisis. There I encounter the “positioning” conundrum.

Paradoxically, it is easier to describe what would happen to the markets in the aftermath of a completely unanticipated and destructive event such as 9/11. We would expect a sharp equities sell-off, a flight to U.S. Treasuries and to defensive currencies such as dollar, swiss franc, and yen. The reason is that if market players are not positioned for this particular event, it is easy to guess what they would do.

But when an event was in the making for five years, the prediction is much harder. The “buy the rumor, sell the fact” paradigm comes into play. If we assume that most of speculative money was already positioned defensively with respect to Greece, any resolution may come as a relief.

But let’s go to the next level. If the speculators anticipate the post-resolution relief rally in Greek bonds and stocks, they may actually not be positoned defensively.

You know that I know that you know…

A parallel begs to be drawn with the Russian crisis of 1998. Russia didn’t default exactly overnight. But market players were anticipating either default or devaluation of ruble, not both. Caught by surprise, over-leveraged hedge funds folded like dominos, liquidating all positions, good or bad. Everything, from swap spreads to implied equity vol to municipal bonds went into a crisis mode.

So the question we have to ask ourselves is not just what exactly going to happen to Greece, but how is the “fast money” positioned.

Greek banks are not opening on Monday.

Stock market is likely not opening.

Virtually nothing should surprise us on Monday morning. Not a huge market commotion, not a relief rally, and not even business as usual.

Generally I am a fan of the concept that “crisis doesn’t happen on schedule”. We have learned it after the Y2K. And we knew in advance, about all the deadline for Greece and the dates for Brussels summit.

As I write this on sunday afternoon in California, the euro is down moderately (1.5-2%) and US Bonds are rallying quite a bit. My usual intuition would be not to get overexcited and stay with my core positions without adding anything. Which happen to short euro and long bonds as all my readers know.

If anything my bias would have been to expect for things to calm down and pull back to normal on Monday.

However, for me China is the enormous extra variable in this equation. I have tweeted earlier that extraordinary measures taken by the PBOC over this weekend indicate to me that might more problems there than it looks from the outside. Indeed, the correction in the stock indices like SHCOMP which are still tremendously up on the year is hardly a disaster by itself. But the aggressive central bank’s response may instill further doubt rather than inspire confidence.

But beware of contagion! Risk aversion in Europe may spill into Asia and converse. And when it comes to positioning in China – I have a feeling – the majority market players expect the government to be able to back-stop any crisis.

This type of confidence has been a path to disaster over and over again in the course of history.

My readers know me as a general global growth and economy bull. I don’t cry “crisis” often. But the confluence of events over last few days is making me view risks as highly elevated.

The dollar chart is no longer parabolic. It’s vertical.

This by itself is not an indicator, that we have to close the long dollar trade. My general feeling is “Why give up on a good trend, while it lasts?”

On January 1st, 2015 I posted that I had reduced my short Yen risk and focused on short Euro. My relatively conservative risk commitment at the beginning of the year allowed me to build a short Swiss (long USDCHF), after the SNB surprise action had sent the currency into the opposite of freefall.

But now both EURUSD and USDCHF trades have moved enough to be considered mature along with USDJPY.

Even the secular dollar bulls, who are calling for EUR to go back to 0.80 and JPY to 150, have to admit that more than half on the move has already taken place.

When EURUSD was at 1.35, it was easy for to say “I will stay short no matter what. If it goes a few % against me, I will just wait it out.” Now there is a lot to lose from 1.05.

So, are you prepared to sit on your short EUR position, if it goes back to say 1.15? Maybe you are. But it is not crazy for even the greatest dollar bulls to think of some risk management. For some it means reducing positions, for some trailing stops. Personally, I prefer the former.

As I am taking some profits on EUR and CHF, my thoughts are turning to currencies that haven’t moved quite as much and still have space to catch up in the devaluation race.

You might have guessed what part of the world I am thinking of from the picture upfront. China, Taiwan, Australia, New Zealand, Korea, and so on.

Australia in fact has already moved a lot as well. But New Zealand, as I have written before, looks very expensive against its larger neighbor. So I have recently decided to swallow the negative carry pill and establish a small NZDUSD short.

China is the focus of raging debates and what is actually going on there is beyond the scope of this post.

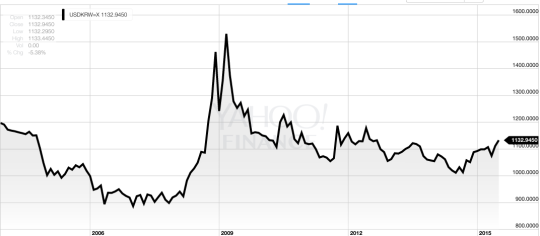

I would like to have a better look at South Korea, which delivered a surprise rate cut last week, confirming its participation in the race to the bottom.

Indeed KRW has weakened somewhat against the US dollar. But the 10% retreat to the highs is not that substantial. If you substitute USD by the currency of their closer neighbor – JPY, you will see a very different picture (lower number means stronger KRW).

So we have a theme similar with China and New Zealand: the carry is not great (though closer to zero in the case of Korea), looks weaker relative to USD, but strong relative to some key counterparties.

I have to confess, I am not at all an expert on Korean economy.

Rather than to analyze specific countries, I want to focus on the general theme. How much downside is really there in being short USDNZD, long USDCNY and USDKRW?

Yes you might have to eat some negative carry, but are you worried about catastrophic appreciation of any of those currencies?

So now that we have (hopefully) booked some profits on easy positive carry trend trades in EUR, JPY, and CHF; is it worth to pay some carry in places where the downside is not that big?

I find it hard to imagine the world in which the broad dollar continues and the “catch-up” currencies do ont devalue as well.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Google Analytics and Tag Manager

This website uses Google Analytics to collect anonymous information such as the number of visitors to the site, and the most popular pages.

Keeping this cookie enabled helps us to improve our website.

Please enable Strictly Necessary Cookies first so that we can save your preferences!